ORGANISATION

FOR ECONOMIC CO-OPERATION

Pursuant

to Article 1 of the Convention signed in Paris on 14th December 1960, and which

came into force on 30th September 1961, the Organisation for Economic

Co-operation and Development (OECD) shall promote

policies

designed:

–

To achieve the highest sustainable economic growth and employment and a rising

standard of living in Member countries, while maintaining financial stability,

and thus to contribute to the development of the world economy.

–

To contribute to sound economic expansion in Member as well as non-member

countries in the process of economic development. And

–

To contribute to the expansion of world trade on a multilateral,

non-discriminatory basis in accordance with international obligations.

The

original Member countries of the OECD are Austria, Belgium, Canada, Denmark,

France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands,

Norway, Portugal, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the

United States. The following countries became Members subsequently through

accession at the dates indicated hereafter: Japan (28th April 1964), Finland

(28th January 1969), Australia (7th June 1971), New Zealand (29th May 1973),

Mexico (18th May 1994), the Czech Republic (21st December 1995),

Hungary (7th May 1996), Poland (22nd November 1996), Korea (12th December 1996)

and the Slovak Republic (14th December 2000).

7

© OECD 2001

There

is a clear trend

in

the OECD area towards

a

knowledge-based economy…

The

ability to create, distribute and exploit knowledge is increasingly

central

to competitive advantage, wealth creation and better standards of

living.

The STI Scoreboard 2001 presents the latest OECD indicators on the

knowledge-based

economy. Many are new, and they are brought together for

the

first time in one publication. As a range of new indicators show, the

knowledge-intensity

of OECD economies is increasing. Investment in

knowledge,

particularly in R&D and software, is rising, as is investment in ICT.

Moreover,

the composition of investment is changing, particularly in R&D

where

a growing proportion is funded by business. Knowledge flows within

and

across OECD economies are increasing as well, as shown by growing

co-operation

in science and innovation, greater international mobility of

high-skilled

workers and continued globalisation of trade and investment.

Information

and communications technologies are also spreading quickly and

support

more rapid knowledge creation and diffusion.

…

which is reflected in the

economic

and innovative

performance

of certain OECD

countries.

The

knowledge-based economy is also reflected in the economic

performance

of several OECD countries. High-technology sectors contribute

to

more rapid growth in some, and the share of these sectors – both in

manufacturing

and services – continues to grow. Moreover, the overall

efficiency

of capital and labour has increased in some OECD countries in the

1990s,

partly owing to more rapid technological progress. Indicators of

patenting

confirm the swift pace of innovation.

Nevertheless,

large differences

continue

to

mark the move towards

a

knowledge-based economy.

While

the overall trends are clear, large differences remain within the

OECD

area. The Nordic countries, notably Finland and Sweden, and the

United

States appear to be in the lead in the transition to a knowledge-based

economy,

as high investment in knowledge, rapid innovation and the pace of

diffusion

of ICT indicate. Countries such as Japan and several large European

countries

appear to lag in important areas, including investment in

knowledge,

innovation and growth of a high-skilled workforce. For certain

OECD

countries, openness to international knowledge flows also seems to

lag.

This suggests scope for further progress. However, the transition to a

knowledge-based

economy requires progress in many areas, and even

countries

that are ahead in many of them lag in others.

New

indicators show that the knowledge-intensity of OECD economies

is

increasing

Investment

in knowledge

is

growing more rapidly than

investment

in

fixed capital…

Investment

in knowledge, defined as public and private spending on

higher

education, expenditure on research and development (R&D) and

investment

in software, accounts for about 4.7% of OECD-wide GDP. It would

exceed

10% of GDP if education expenditure for all levels was included. By

this

measure, Sweden, the United States, Korea and Finland are the four most

knowledge-based

economies. During the 1990s, investment in knowledge

increased

by 3.4% annually in the OECD area, while investment in fixed

capital

increased by 2.2%.

OECD,

STI Scoreboard 2001

…

and ICT has been the most

dynamic

element.

ICT

hardware and software have been the most dynamic area for

investment.

The available data show that it rose from less than 15% of total

non-residential

investment in the business sector in the early 1980s to

between

15% and 35% in 1999. Investment in software accounted for 25-40% of

the

contribution of ICT to overall investment growth.

Investment

in education and

skills

underpins the growth of

a

skilled workforce.

Education

and skills, which underpin the growth of a skilled workforce,

account

for the bulk of investment in knowledge. In 1999, 65% of the

population

aged 25-64 in the OECD area had completed upper secondary

schooling.

The share is more than 20 percentage points higher in the United

States

and Japan than in the European Union. In 1999, 14% of the OECD-area

population

aged 25-64 had university-level education.

Human

resources in science

and

technology are

expanding…

In

1999, there were about 38 million workers (about 25% of the labour

force)

in highly skilled S&T-related occupations in the European Union. The

share

was highest – about one-third – in the Nordic countries (Sweden,

Denmark,

Finland) and in the Netherlands, Germany and Belgium. Human

resources

in science and technology (HRST) grew significantly between 1995

and

1999 in southern Europe, Ireland and Finland. The growth rate of HRST was

similar

in European Union countries and the United States (about 3% annually).

…

as is expenditure for R&D.

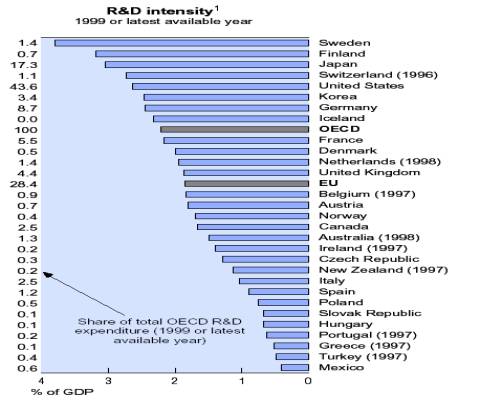

OECD-area

expenditure on R&D has increased considerably over the

past

two decades. It has grown by almost 4% a year and has accelerated since

the

mid-1990s. Most of the increase between 1994 and 1999 was due to the

United

States. During the 1990s, R&D expenditure grew by more than 13%

annually

in Ireland, Mexico and Iceland. In 1999, OECD countries allocated

about

USD 553 billion to R&D, or approximately 2.2% of overall GDP. Since the

mid-1990s,

R&D intensity has increased continuously in Japan and the United

States

and has remained more or less stable in the European Union.

Innovation

relies also on

venture

capital.

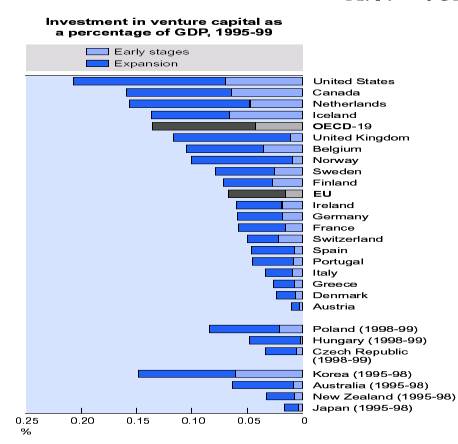

Despite

a recent slowdown, venture capital remains a major source of

funding

for new technology-based firms. Between 1995 and 1999, it amounted

to

0.21% of GDP in the United States and 0.16% of GDP in Canada and the

Netherlands

for early and expansion stages. Almost half of venture capital

investment

in the OECD area is for ICT, representing more than 67% in the

United

States and over 53% in Ireland and Norway. Biotechnology is also of

growing

importance, accounting for the bulk of venture capital investments in

Hungary,

and about 15% in the United States.

The

role of business in R&D is increasing

Business

is the main source of

increased

spending on R&D.

The

business sector is the major source of R&D financing. In 1999, it

provided

more than 60% of domestic R&D funding in OECD countries, a slight

increase

from 1990. Over the decade, the business sector’s share increased

from

57% to 67% of total R&D funding in the United States; it remained stable

in

Japan at around 72% and increased from 52% to 55% in the European Union.

In

most countries, government’s role in funding R&D declined over the 1990s.

More

R&D spending is

directed

towards basic

research…

Most

countries spent a higher share of GDP on basic research in 1998-99 than

in

the early 1980s. Since 1995, the ratio of expenditure on basic research to GDP

has

been flat in the United States, but it has grown in Japan, France and Italy.

Relative

to GDP, Switzerland allocates close to 0.8% of GDP to basic research,

almost

twice as much as the United States or Japan. In Korea, Japan and Ireland, around

one-third of basic research is performed by the business sector.

…

with less going to defence…

During

the 1990s, the share of defence R&D budgets relative to GDP

dropped

in most countries, largely owing to the overall reduction in military

spending.

France, the United States and Sweden experienced the strongest

decline.

Nonetheless, more than half of the US government R&D budget is

allocated

to defence, as is around a third of the total R&D budget in the

United

Kingdom and around a quarter in France and Spain.

…

and more to health…

During

the 1990s, government support for health-related R&D rose

quickly

in Japan (10%) and the United States (8%), with growth rates about

double

that in the European Union (5%). Compared to the European Union

and

Japan, government support for health R&D is high in the United States.

In

2000, it represented about 0.2% of GDP, far above the figures for the

European

Union (0.05% in 1998) and Japan (0.03%). This difference is partly

due

to institutional differences. When appropriate adjustments are made,

however,

Finland, Austria and the Netherlands have health R&D budgets

relative

to GDP similar to that of the United States. The difference in

government

support for health R&D between the United States and the

European

Union also narrows sharply.

…

with a growing share

for

biotechnology.

A

significant and increasing part of health R&D concerns biotechnology.

Data

for biotechnology R&D are currently only available for 20 OECD

countries

and do not include the United States and Japan. They show that,

in

1997, public funding of biotechnology R&D amounted to approximately

USD

3.4 billion. Germany (USD 1.0 bi llion), the United Kingdom

(USD

0.7 billion) and France (USD 0.6 billion) account for the bulk of it.

Belgium

and Canada have the highest ratio of biotechnology R&D to total

government

budget appropriations for R&D (14% and 10%, respectively).

R&D

in the ICT sector also

contributes

significantly

to

overall R&D.

ICT

also accounts for a growing share of overall R&D. Data for 19 OECD

countries

indicate that, in 1998, R&D expenditure for ICT manufacturing was

approximately

USD 96 billion; for the ICT services industries, data for

11

OECD countries show expenditure of USD 18 billion. In 1998, Finland was

the

only country to allocate more than 1% of GDP to ICT-related manufacturing

R&D.

ICT-related R&D intensities of the large European economies are well

below

those of the United States and Japan. In the 1990s, the United Kingdom

is

the only large European country where ICT-related R&D increased slightly

in

manufacturing and services industries (by 1% and 3% a year, respectively).

In

manufacturing, ICT-related R&D decreased in Germany, France and Italy by

1%,

2% and 0.5%, respectively.

Knowledge

flows within and across economies take on greater importance

Innovation

increasingly relies

on

co-operation between firms

and

universities.

The

use and generation of knowledge depend not only on the creation of

knowledge

but also on flows of knowledge within and among economies.

Collaboration

between business and non-business entities is rising, and the

share

of R&D performed by the higher education and government sectors and

funded

by the business sector is increasing. It represented 6.1% and 4.1% of

higher

education and government research, respectively, in 1998. Data from

innovation

surveys show that firms with co-operation arrangements with higher

education

or government institutes account for around 10% of total employment.

International

co-operation in

science

and innovation

is

growing rapidly…

Production

of scientific research and technological know-how also

increasingly

depends on research conducted in other countries. In the mid-

1990s,

27% of scientific publications in the OECD area were the work of

multinational

teams and 7% of patents were the result of international

co-operative

research. In smaller European countries, such as Belgium,

Denmark

and Austria, over 40% of scientific publications have a foreign

co-author.

When intra-EU co-operation is factored out, researchers in the

United

States and the European Union have a similar propensity to

co-operate

with foreign researchers; in Japan, instead, international

co-operation

in science and technology is quite limited.

…

as is cross-border

ownership

of inventions.

More

and more technology is owned by firms from a country other than

the

inventor’s country of residence. In the mid-1990s, an average of 14% of all

inventions

in any OECD country were owned or co-owned by a foreign

resident.

Likewise, OECD countries owned around 15% of inventions made

abroad.

Foreign ownership of domestic inventions is high in several small

OECD

countries, but also in Canada and the United Kingdom, where US

companies

own a large share of inventions. Domestic ownership of foreign

inventions

is also high in small countries; 39% of all inventions owned by

Swiss

residents were invented abroad. In the United States, the share of

foreign

inventions in the patent portfolio is only 13%. Japan and Korea are the

least

internationalised in this respect.

Worker

mobility supports the

flow

of knowledge across borders…

Knowledge

flows also result from migration. In the United States, for

instance,

the largest number of scientists and engineers (S&Es) with S&E

doctorates

who were born elsewhere in the OECD area are from the United

Kingdom

and Canada; relatively few are from Germany or Japan. However,

three

times as many foreign-born scientists are from China and twice as many

from

India as from the United Kingdom. In 1998, for the 14 European countries

as

a whole, non-national HRST amounted to only 3%. However, European

countries

differ widely; Luxembourg employs by far the largest share of

non-nationals

(33%), followed by Austria, Belgium and the United Kingdom.

…

as does student mobility.

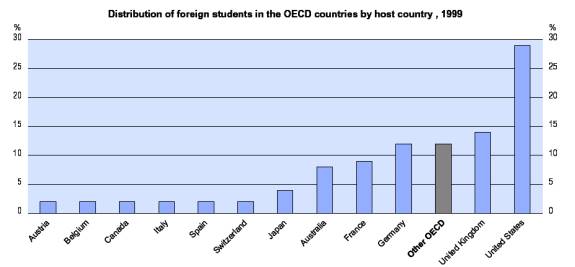

International

mobility of students also represents a potential flow of

qualified

workers. Five countries are host to more than 70% of all foreign

students

in OECD countries. The United States attracts 29% of foreign

students,

followed by the United Kingdom (14%) and Germany (12%).

English-speaking

countries account for over 50% of the OECD total. In

Switzerland,

Australia, Austria, Belgium and the United Kingdom, foreign

students

represent more than 10% of total enrolments. In Korea, Mexico and

Poland,

they account for less than 1%.

The

globalisation of the

knowledge

economy is

apparent

in the rapid growth

of

international transactions.

National

economies also integrate in other ways. Financial transactions

(e.g.

direct investment and portfolio investment) constitute the fastest growing

segment

of international transactions. The upsurge in direct

investment

and portfolio investment was especially rapid in the second half

of

the 1990s. However, such investment flows have proven highly volatile. The

lowering

of trade and non-trade tariff barriers has also contributed to a steady

rise

in international trade.

Trade

is growing rapidly,

particularly

in services…

The

share of trade in international transactions has remained persistently

high,

averaging 15% of OECD GDP in the 1990s. That of trade in goods is four

times

that of trade in services, despite the acceleration of the latter. In the

second

half of the 1990s, international trade in services as a share of GDP

picked

up slightly, partly as the result of the growing tradability of certain

services,

e.g. software, financial services and accounting. The trade-to-GDP

ratio

is only around 10% for the United States, Japan and the European Union

when

intra-EU trade flows are excluded. During the 1990s, the international

trade-to-GDP

ratio grew on average about 2% in the European Union and the

United

States but declined slightly in Japan.

…

and foreign direct

investment

has picked

up

in recent years...

Flows

of foreign direct investment (FDI) have surged in recent years,

owing

to renewed dynamism in the world economy and a favourable

international

investment environment. FDI flows as a percentage of GDP are

high

for Belgium-Luxembourg, New Zealand, Sweden, the Netherlands,

Switzerland

and the United Kingdom. They remain small in Turkey, Korea,

Japan

and Italy. In Germany, Japan and the United Kingdom, outward

investment

greatly exceeds inward investment, while Australia, Hungary,

Poland

and Spain receive more foreign capital than they invest abroad.

…

partly owing to increases in

mergers

and acquisitions.

Mergers

and acquisitions are the most common form of FDI. During the

1990s,

cross-border mergers and acquisitions increased more than five-fold

worldwide

on a value basis. The United States was the main target during the

1995-99

period, attracting on average four times as many deals in terms of

number

than the United Kingdom, the second target country. Germany and

France

took third and fourth place. During the 1990s, the most active sectors

at

global level were oil, automotive equipment, banking, finance and

telecommunications.

Multinational

firms also

account

for a growing share of

activity

in many countries…

The

share of turnover under foreign control in the manufacturing sector

ranges

from about 70% in Hungary and Ireland to under 2% in Japan. In the

period

1995-98, the shares of foreign affiliates in manufacturing turnover rose

almost

everywhere. In terms of manufacturing employment, their shares range

from

around 50% in Ireland, Luxembourg, and Hungary to 1% in Japan. In the

second

half of the 1990s, when manufacturing employment typically declined

in

national firms, it rose in foreign affiliates in all countries except Germany

and

Netherlands. In most cases, this reflected changes of ownership owing to

buy-outs

and acquisitions.

…

and increasingly

in

the services sector

as

well.

The

share of turnover under foreign control in the services sector is over

20%

for Hungary, Belgium, Ireland and Italy. In terms of employment, the

share

of foreign affiliates ranges from 19% in Belgium and around 14% in

Hungary

and Ireland to less than 1% in Japan. In all countries except Norway

and

Finland, the share of turnover of foreign affiliates was greater for

manufacturing

than for services.

Information

and communications technologies are diffusing rapidly

The

knowledge-based economy

is

accompanied by the rapid diffusion of ICT,

especially

the Internet.

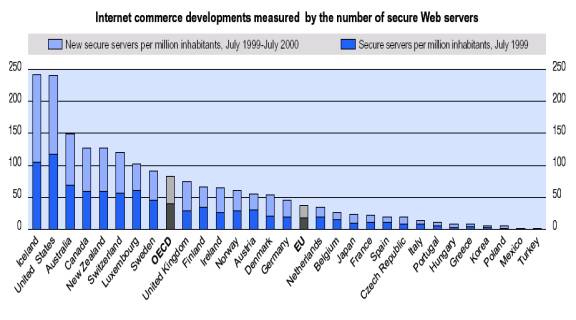

The

diffusion of information and communications technology is a key

enabler

of the knowledge-based economy. Access to ICT has grown rapidly

over

the past years. At the end of 1999, OECD countries had more than one

network

access channel for every two inhabitants and several countries had

more

than one access channel per inhabitant. The Nordic countries maintain a

clear

lead over the rest of the OECD area when connectivity provided by

wireless

networks is taken into account. Internet technologies are diffusing

very

rapidly. At the end of 1999, there were nearly 50 million Internet

subscribers

in the United States, close to 11 million in Japan and in Korea,

9

million in Germany, 7.4 million in the United Kingdom and 6.2 million in

Canada.

A ranking of countries in terms of Internet subscribers per

100

population shows high levels of take-up in Korea, Sweden, Denmark,

Canada,

the United States, Netherlands, Iceland and Norway.

Access

to the Internet is

soaring

in most countries…

Personal

computers are still the main device used by households to access

the

Internet. In most countries for which data are available, more than half of all

households

now have computers. In 2000, there was a noticeable gap between

northern

European countries such as the Netherlands (69%), Denmark (65%) and Sweden (60%)

and southern European countries such as Italy (28%), France (27%) and Turkey

(12%). Internet access in households is soaring everywhere, especially in Italy

where the access rate grew by 144% between 1999 and 2000, as well as in the

United Kingdom (75%), Japan (74%) and France (73%).

…

as is its use, but Internet

transactions

remain limited.

The

share of adults using the Internet from any location is also increasing

rapidly.

More than half of the adult population now uses the Internet in

Sweden

(68%), Denmark (62%), Finland (54%) and Canada (53%). The Internet

is

still mostly used to search for information, and the propensity to carry out

transactions

over the Internet varies widely. In Sweden, 43% of Internet users

purchase

over the Internet, followed by the United Kingdom (33%), the

United

States (30%) and Denmark (29%). Business use of the Internet is

increasing

very rapidly. Internet penetration in businesses with ten or more

employees

has reached 80-90% in the Nordic countries, Australia, Canada, the

Netherlands

and the United Kingdom. In the Nordic countries, over 40% of

employees

use the Internet in their daily work. The use of the Internet to

conduct

transactions, although rising fast, is limited. The value of Internet

sales

in 2000 ranged between 0.4% and 2% of total sales, while electronic sales

(including

those over all computer-mediated networks) reached almost 6% in

the

United Kingdom.

The

rate of diffusion differs

between

users and across

countries…

Internet

penetration in households is strongly affected by household

income.

The difference between Internet access in households belonging to the

lowest

and highest income quartiles is highest in the United States and lowest in

Denmark.

Internet usage rates are much higher in large than in small enterprises

and

vary in different economic sectors. The most intensive business users are

generally

firms in finance and insurance, business services and wholesale trade.

…

partly owing to differences

in

access costs.

A

key determinant of cross-country differences in the diffusion of the

Internet

and electronic commerce is access cost. There are large differences

in

prices of leased lines, which provide the infrastructure for business-tobusiness

electronic

commerce. The Nordic countries have the lowest charges,

at

about one-fifth the OECD average. Differences in Internet access cost for

consumers

are even more marked. At peak times, countries which

traditionally

have had unmetered local calls – Australia, Canada, Mexico, New

Zealand,

the United States – are among the least expensive.

The

structure of OECD economies and of trade reflects the increasing role

of

knowledge

As

knowledge has grown in

importance,

so has the share of

knowledge-intensive

industries…

By

the end of the 1990s, high- and medium-high technology

manufacturing

accounted for about 9% of total OECD value added. The

share

of high- and medium-high technology industries was largest in

Ireland,

where they accounted for over 16% of value added, and in Korea

(12.6%).

Among the G7 countries, Germany and Japan had the largest shares

of

such industries, at 11.7% and 10.7% of total value added, respectively. In

many

OECD countries, including the United States, this sector has grown

rapidly

over the 1990s.

…

and knowledge-intensive

services.

Knowledge-based

“market” services accounted for 18% of total value added

in

the OECD area. Post and telecommunications, finance and insurance and

business

services are typically the most intensive technology users among

market

services. These sectors accounted for almost 25% of total value added in

Switzerland.

Among the G7 countries, the United States and the United Kingdom

had

the largest knowledge-intensive services sector. In Mexico and Greece, this

sector

accounted only for about 10% of value added. If knowledge-intensive

“non-market”

services (education and health) are included, knowledge-intensive

services

account for about 29% of total value added in the OECD area.

The

changing structure

of

OECD economies is also

reflected

in business R&D.

Services

have a much smaller share in R&D than in GDP. In 1998, they

accounted

for about 17% of total business sector R&D in the OECD area, an

increase

of 2% from 1992. Countries differ widely, however. In Norway, 48% of

total

business R&D is carried out in the services sector, 37% in Denmark and

31%

in the United States. Although the share of services R&D increased over

the

1990s in Germany, France and Japan, these countries still have the lowest

share

of services R&D (less than 10%).

The

ICT sector has grown very

rapidly

in several OECD countries.

The

ICT sector makes a substantial contribution to the economy. In 1999, ICT

value

added represented between 5% and 14% of business sector value added in OECD

countries. The importance of ICT supply has been increasing, not only in

countries like Hungary, the Czech Republic and Mexico, which are catching up in

terms of infrastructure, but also in Finland, Sweden, Norway, the Netherlands

and the United Kingdom. In Finland, the ICT sector’s share of value added

increased by 4.7 percentage points over the 1995-99 period. It now represents

over 13% of total business sector value added. The ICT sector is a major source

of employment growth. OECD employment in the sector grew by over 12% in the

1995-99

period, i.e. an average annual rate of over 3% a year, double that of

overall business sector employment. ICT services are driving this growth.

International

trade

in

high-technology goods

is

also rising rapidly…

The

growing importance of knowledge-intensive industries is also visible

in

the structure of OECD manufacturing trade. The share of high-technology

industries

in total OECD trade increased from 18% in 1990 to one-quarter

in

1999. The highest growth rates in OECD manufacturing trade in the 1990s

were

in high-technology industries: pharmaceuticals, radio, television and

communication

equipment and computers. The shares of medium-low- and

low-technology

industries have gradually declined.

…

although only a few OECD

countries

have a strong comparative advantage in

high-technology

industries.

In

spite of the growing importance of high-technology industries in overall

trade,

few OECD countries specialise in high- and medium-high-technology

industries.

In 1999, the structural surplus in these industries represented more

than

15% of total manufacturing trade for Japan, about 7.5% for Switzerland and

around

5% for Germany, Mexico and the United States. A considerable number of OECD

countries still have a strong comparative advantage in medium-low technology and

low-technology industries. The structural surplus of Turkey, New

Zealand

and Iceland in these industries accounted for more than 20% of total

manufacturing

trade. For most OECD countries, these specialisation patterns

have

changed little over the past decade.

Knowledge

and innovation increasingly underpin economic performance

Innovation

is a key driver

of

economic growth…

Recent

patterns show that knowledge and innovation make a large

contribution

to growth. A high share of investment in fixed capital goes for ICT.

Moreover,

the overall efficiency of the use of capital and labour in the

production

process, or multi-factor productivity (MFP), increased rapidly in

Ireland,

Finland, Australia, Canada and the United States in the second half of

the

1990s. More rapid MFP growth points to faster technological progress.

Furthermore,

rapid productivity growth in high-technology sectors such as ICT

has

contributed strongly to growth in several countries.

…

and patenting is

accelerating,

although

differences

among OECD

countries

are large.

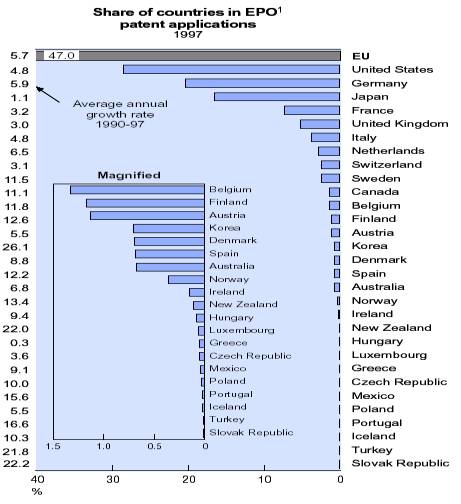

Indicators

of patenting confirm the brisk pace of technological progress.

Over

the 1990-97 period, patent applications at the European Patent Office

increased

annually by 5.7% for the European Union, 4.8% for the United States

and

1.1% for Japan. During the 1990s, growth rates for patents in ICT (8%) and

biotechnology

(10%) for the OECD area were almost twice that of total patent

applications

(5%). Indicators of patent families – patents taken at the European

Patent

Office, the US Patent and Trademark Office and the Japanese Patent

Office

to protect a single invention – show that there were about 32 000 patent

families

in the OECD area in 1995. The United States accounted for about 35%,

followed

by the European Union (32%) and Japan (27%). When population size

is

taken into account, Switzerland patents the most by far in the OECD area. In

1995,

there were close to 100 patent families per million population in

Switzerland,

far above Sweden (74) and Japan (69).